Many buyers come to Hua Hin with one big question stuck in their head. Should I buy a property here to live and enjoy or should I buy it to make money? It sounds like a simple choice. It is not. Picking the wrong one costs people millions of baht every year. Not because Hua Hin is a bad market but because they bought a lifestyle home and expected investment returns or bought an investment unit and expected a dream home.

This guide is for both groups. As a property expert based in Hua Hin I will walk you through how a long term investment is different from a lifestyle purchase. Where each one wins. Where each one loses. And how the smartest buyers in 2026 are mixing both. By the end you will know exactly which path fits your life, your money and your goals. You will also avoid the mistakes most foreign buyers only learn about after they sign.

Why This Question Matters More in Hua Hin Than Anywhere Else in Thailand

Hua Hin is not Phuket. It is not Pattaya. It is not Bangkok. It is a quieter coastal town about 2.5 to 3 hours south of the capital and it attracts a very different kind of buyer. Wealthy Thai families from Bangkok buy weekend homes here. European and Australian retirees pick Hua Hin for its calm beaches, good hospitals and low crime. Bangkok professionals invest here because prices are still 30 to 50 percent lower than Phuket for similar quality properties.

Because of this mix Hua Hin works very well as a lifestyle home. It also works for steady long term investment. But it does not work the same way Phuket does for short term Airbnb style profit chasing. If you understand this from day one you will buy the right property. If you do not you will be disappointed no matter how nice the house looks at the viewing.

What Long Term Investment Really Means in Hua Hin

A long term investment property is one you buy mainly to grow your money. You may never live in it. Your goal is rental income every month plus a higher resale price in 5, 10 or 15 years. The numbers come first. The view, the colour of the kitchen and the size of the garden only matter if they help the property earn more or sell faster.

How a long term investor in Hua Hin thinks

- They study rental demand before they fall in love with a building. Hua Hin condos and villas typically return 5 to 7 percent gross yield per year which beats the Thai national average of 4 to 6 percent.

- They buy what tenants want, not what they want. Tenants want walking distance to the beach, good Wi-Fi, parking, a pool and proximity to Bluport Mall, Market Village or international schools.

- They look at the exit before they look at the entrance. They ask who will buy this from me in 10 years and at what price.

- They pay attention to infrastructure. The proposed Bangkok to Hua Hin high speed rail and the upgraded Hua Hin Airport are expected to push prices up over the next few years.

What a Lifestyle Purchase Really Means in Hua Hin

A lifestyle purchase is a home you buy mainly to enjoy. It might be your retirement villa, your family’s holiday house, your escape from a cold winter back home or the place where you finally slow down. Returns matter but they are not the reason you bought. The reason is the morning walk on the beach, the round of golf at Black Mountain, the dinner with friends at Cicada Market and the calm that Hua Hin gives you that Bangkok and Phuket simply cannot.

How a lifestyle buyer in Hua Hin thinks

- They buy what makes them happy. A private pool, a garden for the dog, a sea view or a quiet soi away from traffic.

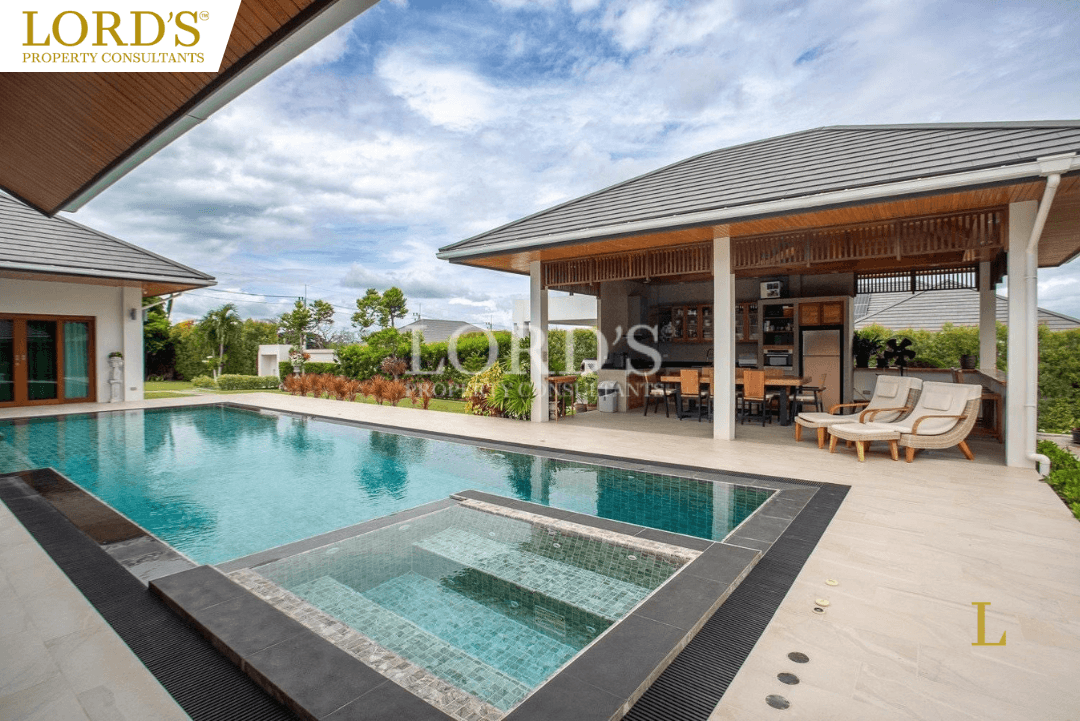

- They pick locations they enjoy living in like central Hua Hin, Khao Takiab, Khao Tao or Pranburi even if the rental yield is slightly lower.

- They are willing to pay a small premium for peace of mind. A well managed gated community, a strong developer and a building that is not 100 percent rental units.

- They think in decades not years. They are not planning to flip. They want to own the home for their own life chapter.

Long Term Investment vs Lifestyle Purchase: A Side by Side Look

Most articles online try to push you toward one answer. This table gives you the honest comparison the way I would explain it to a friend over coffee at a café on Soi 94.

| Decision factor | Long Term Investment | Lifestyle Purchase |

|---|---|---|

| What matters most | Return on money (ROI yield resale) | Personal happiness and use |

| Best property type | Condo near the beach or town centre | Pool villa or low density development |

| Typical budget (THB) | 4 to 10 million | 8 to 25 million+ |

| Ownership type for foreigners | Freehold condo (cleanest path) | Leasehold villa Sap Ing Sith or Thai company |

| Location priority | Walk to beach malls schools | Quiet area sea or mountain view golf nearby |

| Rental plan | Long term tenants or managed short stays | Owner occupied. Rare short rentals when away |

| Expected yield | 5 to 8 percent gross per year | 0 to 4 percent if rented at all |

| Capital growth target | 3 to 7 percent per year infrastructure driven | Steady inflation beating not the main goal |

| Exit plan | Sell in 5 to 10 years to next investor | Hold for life or pass to family |

| Biggest risk | Vacancy or oversupply in wrong location | Overpaying for emotions and illiquid resale |

The 5 Question Self Test: Which Buyer Are You Really?

Before you book a viewing, sit down for ten minutes and answer these five questions. They are the same ones I ask every new client in the office. Be honest. Your wallet will thank you later.

- How many months a year will I actually spend in the property? If it is more than 4 to 5 months you are leaning lifestyle. If it is zero you are an investor.

- If the property never goes up in price will I still feel happy I bought it? A yes means lifestyle. A no means investment.

- Am I buying this in cash or do I need rental income to cover the costs? Needing rental income to break even means you must think like an investor even if you plan to use it sometimes.

- Do I want a fixed exit date such as selling in 7 to 10 years or do I want to keep this for life and pass it to my children? Fixed exit means investment mindset. Forever means lifestyle.

- Would I be comfortable signing a 30 year leasehold contract or do I only want a freehold title in my own name? Freehold only buyers are usually safer with condos and the investment path.

If your answers point clearly to one side that is your path. If they are mixed you are a strong candidate for the hybrid model. That is where the smartest Hua Hin buyers are heading in 2026.

The Hybrid Model: Why More Buyers Now Want Both

A few years ago you had to pick a side. Today the lines are blurring. A growing number of foreign and Thai buyers in Hua Hin use their property six months a year for themselves and rent it out the other six months to cover costs and even turn a small profit. It is one of the most practical strategies the local market has seen in a decade.

How the hybrid model works in practice

- You buy a 2 bedroom condo or small pool villa with strong rental appeal. Walking distance to the beach, good Wi-Fi, secure parking and pet friendly if possible.

- You spend the cooler season (November to March) living there yourself. This is also peak rental season but you keep it for personal use.

- During the hot and rainy months (April to October) a local property manager rents it to long stay tenants, digital nomads or returning expats.

- Net result. 3 to 5 percent yield while still enjoying half the year in your own home. Your dream is funded by the dream itself.

This model only works if you buy the right property in the right location. Lifestyle only homes in remote areas struggle to rent. Pure investor condos in oversupplied buildings can feel cold to live in. The middle is where the magic happens. A trusted local advisor like Lord’s Property Consultants who knows Hua Hin block by block can save you from picking the wrong building.

The True Cost of Owning Property in Hua Hin (Beyond the Sticker Price)

Most online articles only show you the purchase price. That is half the story. Whether you go investment or lifestyle the real cost of ownership over 10 years is much bigger. Here is what to budget for so you do not get surprised.

Upfront costs at the Land Office

- Transfer fee. 2 percent of the appraised value is usually split 50/50 with the seller.

- Stamp duty. 0.5 percent only paid if you do not pay business tax.

- Specific Business Tax. 3.3 percent if the seller has owned for less than 5 years.

- Withholding tax. A small amount based on appraised value and ownership length.

- Legal fees. THB 30000 to 80000 for a standard purchase and absolutely worth it for foreign buyers.

Ongoing costs every year

- Condo common area fees. Typically THB 40 to 80 per square metre per month.

- Villa estate fees in a gated community. THB 2000 to 8000 per month depending on facilities.

- Building insurance, content insurance and pool or garden maintenance for villas.

- Property tax (Land and Building Tax). Small but real and 2026 is bringing tighter rules on vacant properties.

- If you rent it out. Management fees of 8 to 15 percent of rental income plus income tax.

A clear eyed buyer adds these to the purchase price before deciding. A lifestyle buyer treats them as the cost of happiness. A long term investor treats them as the cost of doing business. Both views are correct. You must know the number before you commit.

Foreign Ownership: What You Can and Cannot Buy in Hua Hin

This is where most foreign buyers get stuck. The difference between investment and lifestyle becomes very real here. Thai law does not allow foreigners to own land directly. There are several safe paths and the right one depends on which buyer you are.

Freehold condominium (best for investors)

Foreigners can fully own a condo unit in their own name as long as foreign ownership in the building stays at or below 49 percent of total saleable area. You get a Chanote title deed. You can sell it freely, rent it freely and pass it to your heirs. For long term investors this is almost always the cleanest path.

Registered 30 year leasehold (common for lifestyle villas)

Most pool villas in Hua Hin are sold to foreigners on a 30 year registered lease at the Land Office. A well written lease should clearly state renewal terms, transfer rights and what happens on death. Lifestyle buyers often accept leaseholds because they care about living in the villa not flipping it.

Sap Ing Sith (a newer stronger structure)

Sap Ing Sith is a registered right over a leased asset that gives foreigners much stronger control than a normal lease. It includes the right to sell, mortgage or transfer. It is one of the most important developments for foreign buyers in recent years. Ask your lawyer about it if you are buying a higher value villa.

Thai Limited Company (use with extreme care in 2026)

In early 2026 Thai authorities tightened rules around nominee shareholders and company structures used to hold property. This route is no longer the easy backdoor it once was. Speak to a qualified Thai lawyer before considering it.

Best Areas in Hua Hin for Each Type of Buyer

Hua Hin is not one market. It is many small ones. The same budget buys very different lives in different areas. Here is how I match buyers to neighbourhoods.

Best areas for long term investment

- Central Hua Hin (Soi 94, Soi 88, Khao Takiab Road). High tenant demand, strong walk to beach appeal and top resale liquidity.

- Khao Takiab. Beachfront condos with sea views popular with retirees and short stay guests.

- Wang Pong. A fast growing corridor with new branded projects and capital growth potential.

- Bluport and Market Village area. Lifestyle infrastructure right at the doorstep ideal for long stay expat tenants.

Best areas for lifestyle buyers

- Khao Tao. Quiet with mountain and sea views and low density villa communities popular with retirees.

- Pranburi and Pak Nam Pran. A slower pace and beautiful beaches perfect for second homes.

- Hin Lek Fai. Hillside villas with cooler air and large plots near international schools and Black Mountain Golf.

- Cha Am side (north of Hua Hin). More space, more privacy and lower cost per square metre.

The 2026 Hua Hin Market: What Has Changed and Why It Helps You

If you have been watching the Hua Hin property market from afar here is what is actually moving in 2026 and how each change affects your decision.

- Lower interest rates. The Bank of Thailand cut its rate to 1.25 percent in December 2025 and eased LTV rules through mid 2026. Qualified buyers now have around 8 percent more purchasing power than a year ago.

- Foreign buyers at record share. Foreigners now make up roughly 40 percent of new condo purchases in Hua Hin up from 30 percent five years ago.

- Strong rental yields holding. Gross yields are sitting between 5 and 7 percent beating the national average and matching Bangkok and Phuket without their higher entry prices.

- Infrastructure coming online. The Bangkok to Hua Hin high speed rail expected by 2027 and the upgraded Hua Hin Airport are already pulling forward demand.

- Tighter rules on empty homes. New vacant property tax discussions favour real lifestyle buyers and long term landlords and quietly punish speculative empty units.

Common Mistakes That Cost Buyers Millions of Baht

- Buying a lifestyle villa in a remote area and expecting strong rental income when the renters are not there.

- Buying a pure investment condo in an oversupplied building because the off plan price looked cheap.

- Skipping a Thai property lawyer to save THB 50000 and then losing millions to a bad title check.

- Using a Thai company structure without understanding the 2026 enforcement changes.

- Forgetting that foreign buyers usually pay cash in Thailand. The resale buyer pool is smaller and slower.

- Not planning the exit before signing. Always ask who my buyer is in 10 years and how I will reach them.

How to Make the Final Decision (A Simple 4 Step Framework)

- Be honest about your life stage. Are you retiring, semi retiring, building wealth or diversifying? Each stage points to a different property.

- Set a clear money goal. Write down in 10 years this property should give me X. The X tells you investment or lifestyle instantly.

- Visit Hua Hin in the low season (June to September), not just the high season. You see the real Hua Hin, the real tenant flow and the real you.

- Work with a local expert who knows Hua Hin block by block, not just a Bangkok based agent with a glossy brochure. The wrong building can lose you years of growth.

Quick Answers to the Questions Buyers Search Most

Is Hua Hin a good place for long term property investment?

Yes for stable steady growth and not for quick flips. Hua Hin offers rental yields of 5 to 7 percent and annual price growth of 3 to 7 percent supported by retirees, expats and Bangkok weekenders. If you want fast capital gains, other markets may suit you better. If you want reliability and a real tenant base Hua Hin is one of Thailand’s safest bets.

Can foreigners own property in Hua Hin?

Foreigners can fully own a condominium in their name as long as the building stays under the 49 percent foreign ownership cap. For villas with land foreigners typically use a registered 30 year leasehold or newer structures like Sap Ing Sith. Direct land ownership by foreigners is not allowed under Thai law.

Is it better to buy a condo or a villa in Hua Hin?

Condos are better for investment. Easier foreign ownership, lower entry price, simpler resale and stronger rental yield. Villas are better for lifestyle. More space, private pools, pet friendly and a true retirement feel. Many buyers around the 10 million baht mark feel this divergence the strongest.

What is the average rental yield for Hua Hin property?

Gross rental yields in Hua Hin generally fall between 5 and 7 percent per year. Beachfront and central locations tend to score at the top of that range. Villas in quieter areas yield a little less but enjoy more stable long term tenants.

Is Hua Hin better than Phuket or Pattaya for investment?

Hua Hin gives you better stability, lower volatility, more local Thai demand and prices that are 30 to 50 percent cheaper than Phuket for similar quality. Phuket may give higher short term Airbnb income but with more competition and more risk. For long term owner friendly investing Hua Hin is hard to beat.

Should I retire in Hua Hin or just buy a holiday home?

If you plan to spend more than 4 to 5 months a year in Thailand, retiring or semi retiring in Hua Hin usually makes more financial sense than keeping a part time holiday home. The cost of living is lower than Bangkok. Healthcare is excellent. The retirement visa requirements are among the most accessible in the region.

How long should I hold a property in Hua Hin before selling?

A minimum of 5 years is usually best to avoid the Specific Business Tax of 3.3 percent and to ride out short term market wobbles. Most successful investors hold for 7 to 10 years which lets infrastructure projects and inflation work in their favour.

What are the biggest risks of buying in Hua Hin?

The main risks are choosing the wrong location with low rental demand, using a weak legal structure, buying in an oversupplied off plan project and underestimating ongoing costs. All four are avoidable with a good lawyer, a local agent and a clear plan written down before you sign.

Conclusion: Choose the Buyer You Actually Are

Long term investment and lifestyle purchase are not enemies in Hua Hin. They are two valid doors into the same beautiful coastal market. The mistake is walking through both doors at the same time. Buying a lifestyle home and silently hoping it pays you back like an investment. Or buying an investment unit and slowly turning it into a personal home you can never sell.

Sit with the 5 question self test. Know your numbers. Pick your area. Use the right legal structure. Plan your exit before you plan your housewarming. Do these five things and Hua Hin will reward you whether your reward is a steady rental cheque, a quiet retirement or a clever hybrid of both.

When you are ready to take the next step, work with a property expert who lives here, knows every soi and tells you the truth about a building even when it costs them a sale. That is how you turn a big decision in a foreign country into the best move you ever made.

Beteiligen Sie sich an der Diskussion